All Categories

Featured

Table of Contents

When you make interest in an annuity, you generally do not need to report those profits and pay earnings tax on the incomes every year. Growth in your annuity is insulated from individual earnings taxes.

While this is an overview of annuity taxation, seek advice from a tax professional before you make any kind of decisions. Annuity contracts. When you have an annuity, there are a variety of details that can influence the taxation of withdrawals and income settlements you get. If you put pre-tax cash into an individual retirement account (INDIVIDUAL RETIREMENT ACCOUNT) or 401(k), you pay tax obligations on withdrawals, and this holds true if you money an annuity with pre-tax money

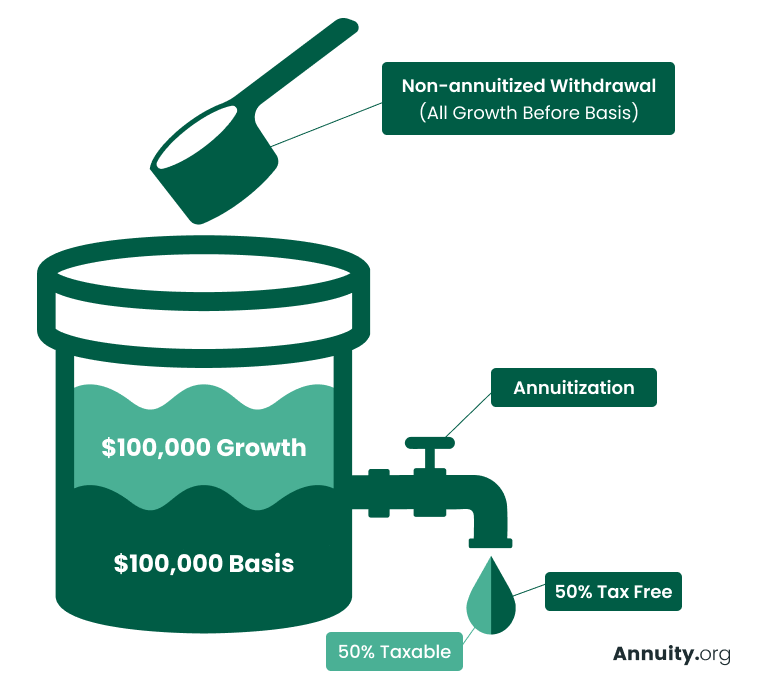

If you contend the very least $10,000 of revenues in your annuity, the entire $10,000 is dealt with as earnings, and would typically be exhausted as average revenue. After you wear down the incomes in your account, you receive a tax-free return of your original round figure. If you transform your funds into a guaranteed stream of earnings repayments by annuitizing, those settlements are split right into taxed parts and tax-free parts.

Each payment returns a portion of the money that has currently been exhausted and a section of interest, which is taxable. If you receive $1,000 per month, $800 of each payment might be tax-free, while the remaining $200 is taxable revenue. Eventually, if you outlast your statistically determined life span, the entire quantity of each repayment might become taxed.

Because the annuity would certainly have been moneyed with after-tax cash, you would not owe taxes on this when taken out. In basic, you have to wait until at least age 59 1/2 to take out profits from your account, and your Roth must be open for at least five years.

Still, the other features of an annuity might exceed revenue tax obligation therapy. Annuities can be devices for delaying and managing tax obligations.

Inherited Tax-deferred Annuities taxation rules

If there are any kind of penalties for underreporting the earnings, you could be able to request a waiver of fines, but the rate of interest usually can not be forgoed. You may be able to organize a layaway plan with the internal revenue service (Long-term annuities). As Critter-3 said, a local expert might be able to aid with this, but that would likely lead to a bit of added expense

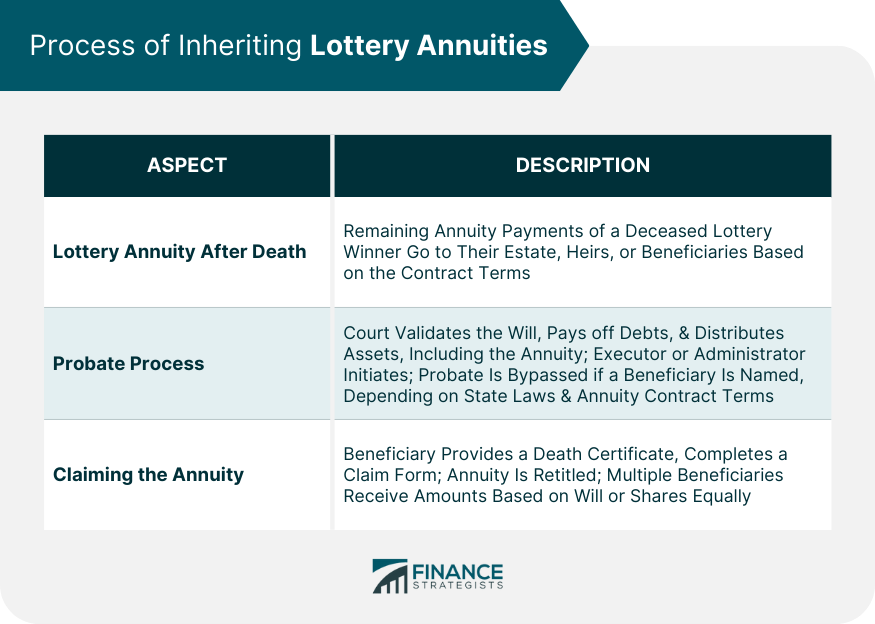

The original annuity contract holder need to consist of a death benefit provision and name a recipient - Annuity interest rates. There are different tax effects for spouses vs non-spouse recipients. Any kind of recipient can choose to take an one-time lump-sum payment, nevertheless, this includes a hefty tax obligation concern. Annuity beneficiaries are not restricted to people.

Fixed-Period Annuity A fixed-period, or period-certain, annuity guarantees repayments to you for a certain size of time. For instance, payments might last 10, 15 or 20 years. If you die during this time, your chosen recipient receives any type of remaining payments. Life Annuity As the name suggests, a life annuity assurances you settlements for the remainder of your life.

Taxation of inherited Flexible Premium Annuities

If your agreement consists of a survivor benefit, staying annuity payments are paid to your recipient in either a round figure or a collection of settlements. You can pick someone to receive all the offered funds or numerous people to get a portion of continuing to be funds. You can additionally select a not-for-profit company as your recipient, or a count on developed as part of your estate strategy.

Doing so allows you to maintain the exact same choices as the initial owner, including the annuity's tax-deferred standing. Non-spouses can also inherit annuity settlements.

There are 3 major means beneficiaries can obtain inherited annuity payments. Lump-Sum Circulation A lump-sum circulation enables the recipient to receive the agreement's entire continuing to be value as a single repayment. Nonqualified-Stretch Arrangement This annuity contract provision allows a beneficiary to receive repayments for the rest of his or her life.

Any beneficiary consisting of spouses can choose to take a single swelling sum payment. In this case, taxes are owed on the entire difference in between what the initial proprietor spent for the annuity and the death advantage. The swelling sum is tired at normal income tax rates. Swelling sum payments carry the highest tax burden.

Spreading repayments out over a longer period is one means to prevent a huge tax bite. For instance, if you make withdrawals over a five-year duration, you will owe tax obligations only on the boosted worth of the portion that is taken out in that year. It is likewise much less likely to push you into a much greater tax obligation bracket.

Inherited Variable Annuities tax liability

This supplies the least tax exposure however additionally takes the longest time to get all the cash. Multi-year guaranteed annuities. If you have actually inherited an annuity, you typically need to choose about your death advantage rapidly. Choices concerning exactly how you wish to get the cash are usually last and can not be transformed later on

An acquired annuity is a monetary product that enables the beneficiary of an annuity agreement to continue obtaining payments after the annuitant's death. Inherited annuities are frequently utilized to offer revenue for enjoyed ones after the fatality of the primary breadwinner in a family members. There are 2 kinds of acquired annuities: Immediate acquired annuities begin paying out right away.

Tax-deferred Annuities death benefit tax

Deferred acquired annuities allow the recipient to wait until a later date to begin receiving repayments. The ideal point to do with an acquired annuity depends on your economic scenario and needs.

It is necessary to talk with an economic advisor prior to making any choices concerning an acquired annuity, as they can aid you determine what is ideal for your specific circumstances. There are a few dangers to consider prior to purchasing an inherited annuity. You should recognize that the government does not ensure inherited annuities like various other retirement products.

Inherited Annuity Death Benefits taxation rules

Second, inherited annuities are commonly complicated financial items, making them hard to recognize. Talking to a monetary consultant before spending in an inherited annuity is essential to guarantee you totally understand the threats included. Ultimately, there is always the danger that the value of the annuity can go down, which would certainly decrease the quantity of cash you obtain in payments.

{kind=link}

Table of Contents

Latest Posts

Highlighting the Key Features of Long-Term Investments A Closer Look at How Retirement Planning Works What Is the Best Retirement Option? Pros and Cons of Various Financial Options Why Fixed Income An

Breaking Down Annuities Variable Vs Fixed Key Insights on Fixed Interest Annuity Vs Variable Investment Annuity Breaking Down the Basics of Investment Plans Features of Smart Investment Choices Why Wh

Breaking Down Fixed Vs Variable Annuities A Closer Look at Annuities Fixed Vs Variable What Is the Best Retirement Option? Benefits of Choosing the Right Financial Plan Why Choosing the Right Financia

More

Latest Posts